What Actually Changes on July 24?

Section 122 of the Trade Act lets the US president impose temporary import surcharges for up to 150 days. On February 24, 2026, a uniform 10% tariff took effect on most imports, with a hard expiration set for July 24.[1]

That deadline is now days away. The replacement framework, a proposed Section 301 structure, is taking shape. USTR is investigating 60 countries, with proposed rates of 10% for nations that have signed reciprocal trade agreements and 12.5% for those that have not.[2]

Here is why that 2.5 percentage point gap matters: on billions of dollars in annual apparel trade, it translates to hundreds of millions in cost variance. Countries with signed bilateral deals (Bangladesh, Cambodia) enter the next phase with a settled rate. Countries without deals (Sri Lanka, and potentially others still negotiating) face a pricing disadvantage the moment the deadline passes.

The policy details will keep shifting. What will not shift is the pattern: sourcing costs now come with a geopolitical premium that did not exist five years ago.

The Map Changed. The Supply Chain Didn’t.

On the surface, the numbers suggest a rapid decoupling from China. US apparel imports from China fell 45.9% year-on-year in the first quarter of 2026. China’s share of US apparel imports has dropped to roughly 9.7%, down from nearly 18% before the tariff escalation.[3] Vietnam now holds the top spot at $4.4 billion in Q1 exports, up 4.7%. Cambodia surged 16.3%.

The map of final assembly has genuinely shifted.

But final assembly is only the last step. New research from the University of Vienna, published in the Journal of Economic Geography, tracked what happened upstream, and the picture looks different.[4] China’s share of global fabric exports rose to 44% by 2022, even as garment production dispersed across new geographies. In synthetic and blended fabrics (the dominant materials in modern activewear) China’s share reached 49%.

Across five leading apparel export countries, fabric and yarn from China account for more than 60% of total textile imports. China holds more than one-third of global export share across key accessories categories: trims, buttons, zippers, elastic. No other single country exceeds 10% in any accessory category.

The researchers put it plainly:

“What the industry frames as supply chain resilience is, in practice, risk management within a structure that remains materially dependent on Chinese inputs.”

There is a reason for this. An apparel assembly factory costs about $1 million to establish. A textile mill costs a minimum of $50 million, and frequently exceeds $200 million. The capital barrier for moving fabric production is an order of magnitude higher than the barrier for moving sewing lines. And the ecosystem (the variety of blends, the speed of new yarn development, the cluster density of accessory suppliers) cannot be replicated by opening a single mill.

China lost 53% of its US apparel sales in dollar terms, according to TexPro data. But it sold $8.5 billion in fabric to its rivals during the same period.[5] The last sewing step moved. Everything before it stayed.

What Happens When Polyester Costs 30% More Overnight?

Tariffs are not the only supply shock hitting activewear right now.

The conflict in Iran and the effective closure of the Strait of Hormuz, through which roughly 21% of global oil passes, has disrupted the petrochemical inputs that polyester depends on. Monoethylene glycol (MEG) and purified terephthalic acid (PTA), the two primary feedstocks for polyester production, have each risen approximately 30% since the conflict escalated in early 2026.[6]

In Surat, India’s textile hub, polyester staple fiber jumped from 100 to 126.5 rupees per kilogram, a 26.5% increase. Coats Bangladesh, one of the region’s largest thread suppliers, announced a 15.5% price increase in April. Zhejiang-based analysts project that apparel retail prices will rise 5% to 15% as these input costs work their way through the chain.[7] Nike and Adidas have both flagged cost pressure in recent communications.

Polyester accounts for roughly two-thirds of global textile fiber output. Your leggings, your sports bras, your compression tops. Most start with the same petrochemical feedstocks now disrupted by a conflict thousands of miles from any sewing line.

This is why “find the cheapest country” math breaks. Your landed cost is not just labor plus tariff plus freight. It is also your exposure to raw material volatility, and that exposure depends on how integrated your supplier’s supply chain actually is, not just where the final stitch happens.

Can Your Factory Do Fast Turnaround AND Volume?

One thing we have learned from working with brands across four continents: different production bases are built for different jobs.

Vietnam excels at high-volume basics. Bangladesh dominates knitwear and denim at scale. Cambodia is gaining ground in simple cut-and-sew categories. China (and this is the part that gets lost in tariff headlines) remains the only place where complex fabrics, fast turnaround, and small-batch flexibility coexist at industrial scale.

The University of Vienna researchers found something telling in their interviews: lead firm fabric managers confirmed that “only China can consistently supply novel yarn blends and fabric types at short notice and scale.” This is not a marketing claim. It is an operational constraint that procurement teams run into every season.

What we see on our own factory floor maps directly to this. A D2C founder testing her first yoga bra design needs 200 pieces in four sizes, with a custom fabric blend that feels like Nulu but costs less. A mid-market brand scaling from 2,000 to 20,000 units needs the same factory to handle both the test batch and the volume run without quality drift. A premium label developing an eco-line needs GRS-certified recycled nylon paired with bio-based packaging, all from a supplier who can do the R&D without demanding a 5,000-piece commitment upfront.

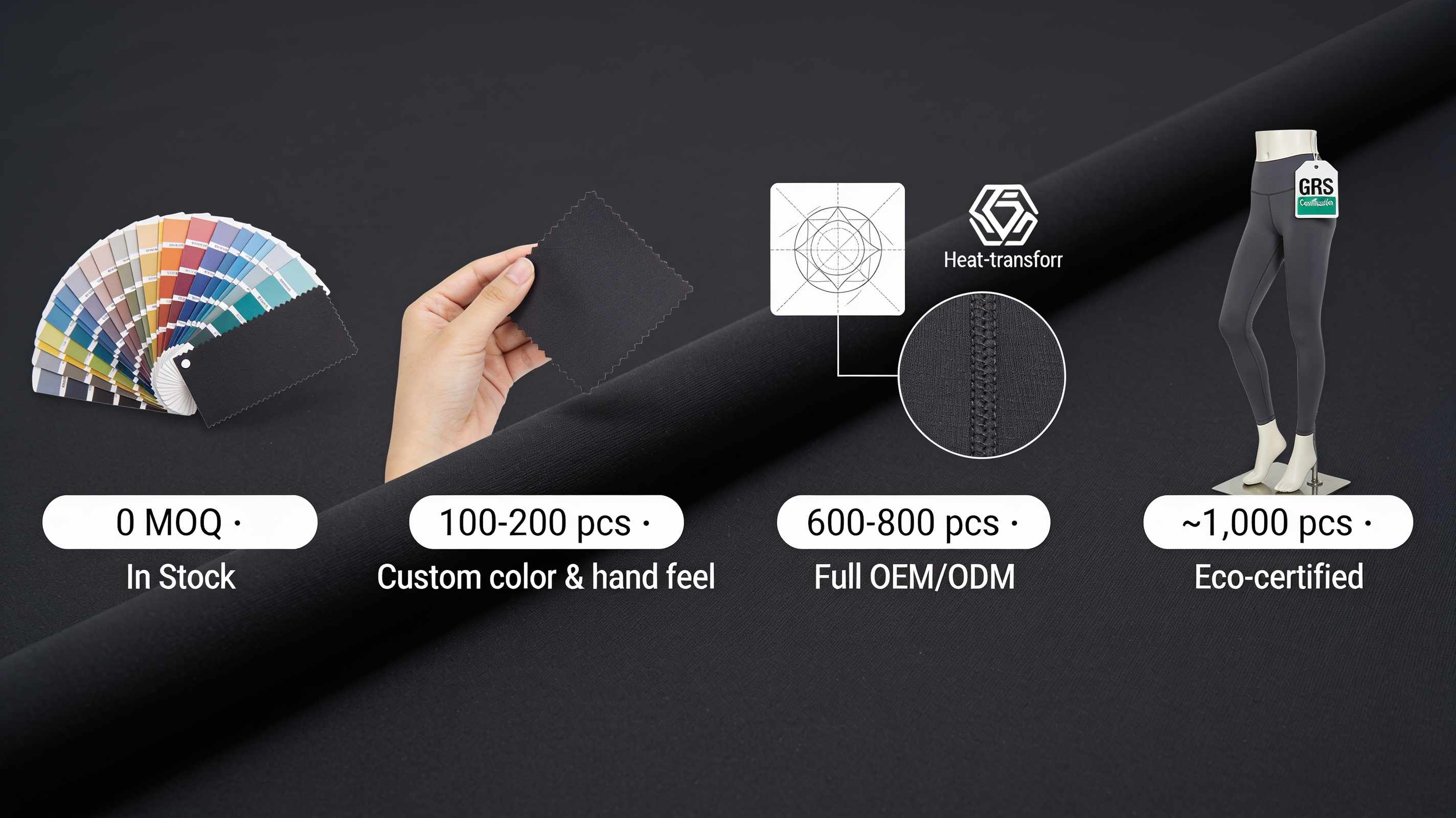

These are three different jobs. They require different production modes. And they all happen inside the same factory, on the same quality system, because the factory was built to handle all four tiers (from zero-MOQ stock items through fabric customization, full OEM, and eco-certified lines) under one roof.[8]

The sourcing question is not “which country is cheapest.” It is “which supplier structure matches where my brand is now, and can it grow with me?”

The Production Math That Tariffs Don’t Capture

Here is a math problem that does not fit on a standard sourcing spreadsheet.

When you are producing across multiple styles and sizes at scale, quality variance costs more than any tariff differential. A half-shade color drift between production batches triggers returns. A seam tension variance that shows up after three washes generates chargebacks. A fabric hand feel that is 90% right but not 100% generates customer reviews that outlive any single season. The per-unit cost of getting it wrong is almost always higher than the per-unit cost of the tariff.

This is why category matters more than country. A $5 basic cotton tee and a $45 compression legging with four-way stretch and flatlock seams are two completely different manufacturing problems. They require different fabric ecosystems, different machine configurations, different skill profiles on the sewing line. A factory cluster that spent 20 years optimizing for the first will not suddenly deliver the second, no matter how attractive the tariff rate looks.

The brands we see making the sharpest sourcing decisions treat their supply chain as a portfolio. Core technical pieces go to factories with deep synthetic fabric expertise. Volume basics go to the most cost-efficient base for those categories. Quick replenishment runs through a nearshore hub. No single country wins every category. No single factory does either.

This is not an argument for or against any particular sourcing destination. It is an argument for making sourcing a category-by-category decision instead of a blanket relocation. Match the product to the production base that is structurally built for it. Time your diversification to your growth stage, not to a headline.

Three Questions to Ask Before You Move

If you are evaluating where to place production for the back half of 2026, here are three questions we have seen the sharpest procurement teams ask before they commit.

First: Is This Product Category Actually Right for the New Location?

A country that produces excellent basic cotton knitwear at scale may not have the synthetic fabric ecosystem to handle a compression legging with four-way stretch and flatlock seams. The fabric supply chain matters more than the labor cost. If your new factory is importing Chinese fabric anyway, you have not diversified your risk. You have just added a shipping leg.

Second: Are You Planning for 15-28 Months, or Are You Planning for Six?

Industry data shows that moving a meaningful share of production to a new country takes 15 to 28 months from initial supplier discovery to stable volume output.[9] Brands that try to compress this into a single season usually end up with three problems at once: delayed deliveries, inconsistent quality, and constant firefighting. The timeline is not a suggestion. It is how long it takes for a new supplier relationship to become reliable.

Third: Can Your Supplier Execute, Not Just Audit Well?

Compliance certificates on a wall are not the same as on-time, on-spec delivery. A factory that passes an audit but cannot maintain quality across 500,000 units, or cannot turn a sample in 10 days when your launch deadline shifts, is not a partner. It is a risk.

We have spent 13 years watching brands navigate these decisions. The ones that win do not pick the cheapest country. They pick the right factory for where they are now, and they build a supplier relationship that can handle where they are going.

ZIYANG is an activewear OEM/ODM manufacturer based in China, producing for 90+ brands across 70+ countries since 2013. We write about what we see from the factory floor.

References

- Textile Today, “Vietnam faces tariff turning point as July 24 deadline nears,” July 2026. textiletoday.com.bd

- Fibre2Fashion, “Trump’s August 1 tariff reset fills the Section 122 vacuum,” July 2026. fibre2fashion.com

- Globaltextiles.com, “U.S. Textile and Apparel Imports Fall 12% in Q1 2026, Vietnam Remains Top Supplier,” 2026. globaltextiles.com

- Maile, F. & Staritz, C., “Lead Firm Strategies in the Global Textile and Apparel Industry,” Journal of Economic Geography, 2026. doi.org; cited via texfash.com

- Fibre2Fashion, “China lost 53% of US apparel sales, but sold rivals $8.5 bn in fabric,” July 2026. fibre2fashion.com

- FashionNetwork, “Iran war hits Asia’s polyester suppliers to global fast fashion,” 2026. fashionnetwork.com

- 21st Century Business Herald, April 2026. 21jingji.com

- ZIYANG company profile: four-tier production ladder. Stock Items (0 MOQ), Fabric Custom (100-200 pcs), Full OEM/ODM (600-800 pcs), Eco Fabric Line (~1,000 pcs).

- NewBuyingAgent, “Why China + 1 Strategies Fail,” 2026. newbuyingagent.com

Post time: Jul-15-2026